When you pick up a prescription, you might see two options: the brand-name drug you recognize from TV ads, or a much cheaper generic version with a plain label. It’s natural to wonder - if they’re both supposed to do the same thing, why is one so much cheaper? The answer isn’t about quality. It’s about competition, cost structure, and how the system works behind the scenes.

Same Medicine, Different Price Tag

Generic medications contain the exact same active ingredients as their brand-name counterparts. They work the same way in your body. The FDA requires them to match brand-name drugs in strength, dosage, safety, and effectiveness. That’s not marketing talk - it’s a legal requirement. A generic version of lisinopril, for example, isn’t a weaker version of Zestril. It’s the same molecule, the same effect, the same side effects - just without the fancy packaging and billion-dollar ad campaigns. So why does a 30-day supply of brand-name Lipitor cost $300 while generic atorvastatin runs $12? The difference isn’t in the pill. It’s in what came before it.How Brand-Name Drugs Get Their Price

Developing a new drug isn’t cheap. Companies spend an average of $2.6 billion and over a decade to bring a single new medication to market. That includes everything from lab research to clinical trials involving thousands of patients. When a drug finally gets FDA approval, the company gets a patent - usually 20 years from the date it was filed. But because the clock starts ticking before human trials even begin, the actual time a company has to sell exclusively is often just 7 to 12 years. During that window, they charge whatever the market will bear. Why? Because they have no competition. There’s only one source for that exact formula. That’s when you see prices like $1,400 for a 30-day supply of lurasidone (Latuda). The company isn’t just recovering R&D costs - they’re making back their investment and funding future projects. That’s the trade-off: innovation is expensive, and patients pay for it upfront.How Generics Slash the Cost

Once the patent expires, any company can apply to make a generic version. They don’t need to repeat expensive clinical trials. Instead, they file an Abbreviated New Drug Application (ANDA) with the FDA. All they have to prove is that their version delivers the same amount of active ingredient into the bloodstream at the same rate as the brand. That’s called bioequivalence. The testing is rigorous, but it costs a fraction of what it takes to develop a new drug - often under $1 million. That’s the first big cost saver. No R&D. No marketing. No sales reps visiting doctors. No TV commercials. That’s why the average generic drug costs 80% to 85% less than the brand-name version. But here’s where it gets even better: competition. Once one company enters the market with a generic, others follow. The FDA approved 700 generic drugs in 2022 alone. Each new manufacturer drives prices down further. In markets with three or more generic makers, prices drop to about 15%-20% of the original brand price within three years. In some cases, like pemetrexed (Alimta), prices fell from $88 per mL to under $10 - a 90% drop.

What This Means for Your Wallet

For patients, the savings are immediate. The average copay for a generic prescription is $6.16. For brand-name drugs? $56.12. That’s nearly nine times more. Over 93% of generic prescriptions cost under $20. Compare that to just 59% of brand-name prescriptions. GoodRx data shows real-world savings: 67% off depression meds, 58% off blood pressure drugs, 57% off weight loss pills. Some erectile dysfunction medications now cost less than $18 a month as generics. For people on high-deductible plans, paying cash for generics often beats using insurance - especially when insurance hasn’t kicked in yet. A 2023 study found that patients who compared prices across pharmacies saved an average of $287 a year just by choosing the cheapest generic option. That’s not a small amount. It’s a month’s worth of groceries. Or a utility bill. Or a prescription co-pay that used to be unaffordable.Not All Generics Are Created Equal

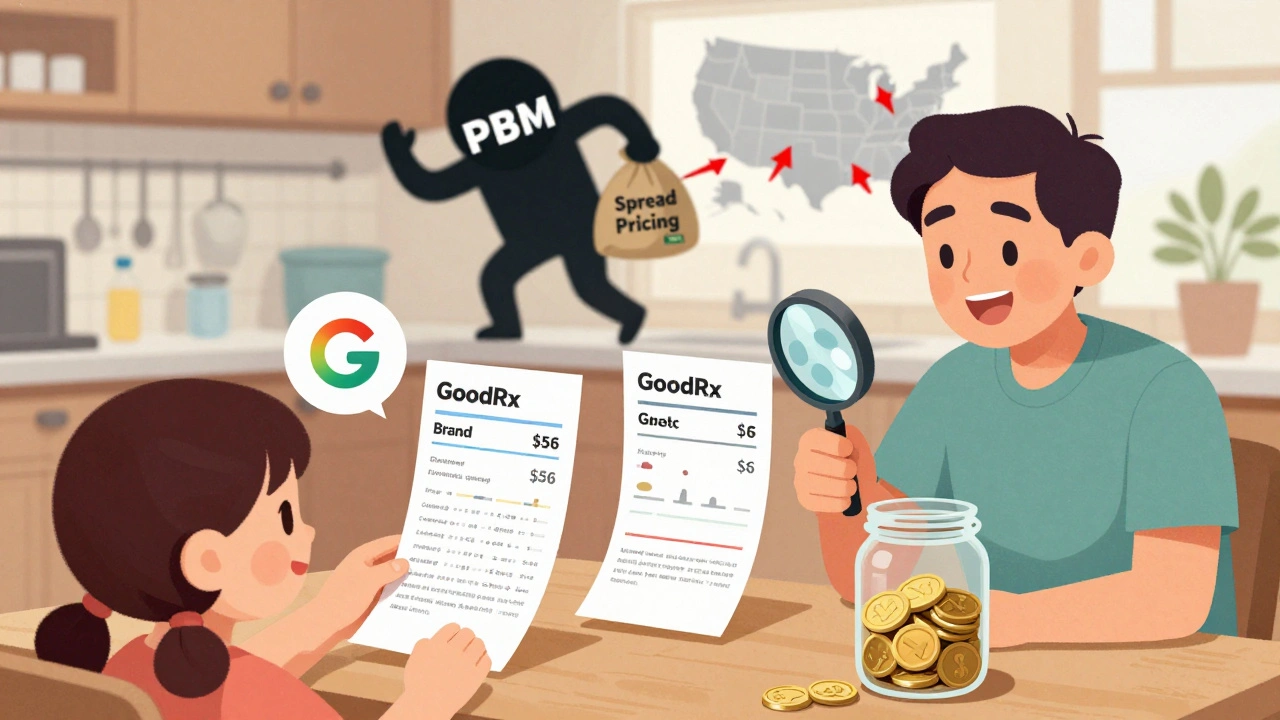

Here’s the catch: not every generic is cheap. Some high-cost generics exist - and they’re not always the best deal. A 2022 study in JAMA Network Open found that certain generic drugs were priced 15.6 times higher than other equally effective alternatives. In Colorado, replacing just 45 of these expensive generics with cheaper ones saved $6.6 million in a single year. Why? Because pharmacy benefit managers (PBMs) sometimes push higher-priced generics onto formularies. They make money off the difference between what they charge insurers and what they pay pharmacies - a practice called “spread pricing.” If a generic costs $50 to make but the PBM charges the insurer $80, they pocket the $30. The patient pays the same copay regardless. So even though it’s labeled “generic,” it’s not helping your budget. That’s why checking prices before filling your prescription matters. A drug labeled “generic” might still be more expensive than another generic version - or even cheaper than your insurance copay.How to Get the Best Deal

You don’t need a degree in pharmacology to save money. Here’s how to make sure you’re getting the lowest price:- Ask your doctor to write “dispense as written” on your prescription. That gives your pharmacist the legal right to substitute a generic if one is available.

- Use free tools like GoodRx or SingleCare. Enter your drug name, your zip code, and see what local pharmacies charge. Often, the cash price is lower than your insurance copay.

- Consider mail-order pharmacies for maintenance medications like blood pressure or diabetes drugs. Many offer 90-day supplies at lower rates.

- If you’re uninsured or on a high-deductible plan, check the Mark Cuban Cost Plus Drug Company. It doesn’t carry every drug yet, but for the ones it does, prices are often 50-80% lower than retail.

- Ask your pharmacist: “Is there a cheaper generic alternative?” They know which ones are in stock and which ones are being discounted.

John Filby

December 5, 2025 AT 04:29Elizabeth Crutchfield

December 6, 2025 AT 06:08Ben Choy

December 7, 2025 AT 18:33Emmanuel Peter

December 9, 2025 AT 17:44Ashley Elliott

December 9, 2025 AT 21:34michael booth

December 11, 2025 AT 07:56Alex Piddington

December 11, 2025 AT 21:21Libby Rees

December 12, 2025 AT 15:05Dematteo Lasonya

December 13, 2025 AT 23:09Rudy Van den Boogaert

December 15, 2025 AT 10:26Gillian Watson

December 16, 2025 AT 02:40Jordan Wall

December 17, 2025 AT 15:00